OECD reports rising degree attainment and strengthening growth for international mobility

The annual Education at a Glance report from the Organisation for Economic Co-operation and Development (OECD) highlights that more people are now earning degrees than ever before.

Looking across OECD countries – a group of 36 advanced economies that includes the entire G7 – the report notes that 44% of 25–34-year-olds now hold tertiary degrees, a significant increase over the 35% that had degrees as of 2008.

“The demand for higher-order skills and competencies is both economic and social,” says OECD Secretary-General Angel Gurría. The OECD finds that tertiary-educated adults are more insulated against the risk of long-term unemployment and that, as of 2018, their employment rate was 9% higher than adults with only secondary education.

Similarly, young tertiary-educated adults (25–34-year-olds) earn 38% more than their peers with secondary qualifications. This gap widens with age, with 45–54-year-olds with tertiary qualifications earning 70% more than their secondary-educated peers.

The OECD finds that the expansion of higher education across the OECD has been supported by increasing funding levels from 2005 to 2016. During this period, spending on tertiary education increased by 28% in OECD countries – more than double the overall enrolment increase of 12% over the same time. “However,” the report adds, “both the number of students and total spending have increased at a slower pace since 2010.”

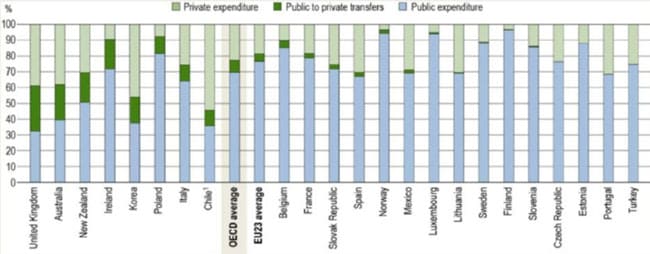

In terms of sources of funding, public funding sources account for 66% of spending on tertiary education across OECD countries. Private sources, mainly tuition fees paid by students, provide the balance.

There are notable variations from this average. For example, in Australia, Chile, Japan, Korea, the UK, and the United States, more than 60% of total tertiary expenditure derives from private sources (and from tuition revenues in particular).

“Between 2010 and 2016,” adds the OECD, “the share of expenditure coming from private sources ... increased by 3%, while the share from public sources decreased by the same amount on average across [member] countries.”

Looking ahead, the OECD sees a more agile and adaptive tertiary sector taking shape. “While widespread access to information has made it easier to learn than ever before, it has also accelerated the pace of change,” adds Mr Gurría. “[This leaves] many wondering how to adapt and struggling to keep up. Globalisation, while providing many opportunities, has also triggered fierce competition for skills.”

“Countries have responded to these challenges by expanding access to education and learning ... As market demand for skills evolves quicker than some educational institutions may anticipate, many of these institutions are promoting flexible pathways into tertiary education and seeking partnerships with other players, including employers, industry and training institutions.”

Charting international mobility

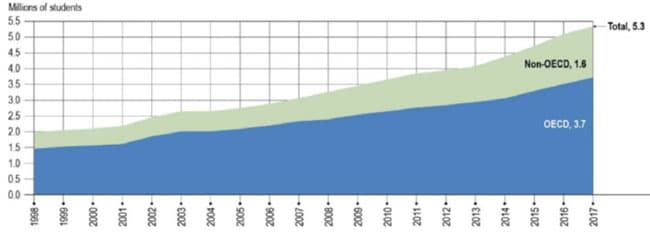

Along with its detailed data and analysis of education in OECD states, Education at a Glance also provides an overview of the broad patterns of international mobility. In particular, and as reflected in the chart below, the report describes a pattern of substantial growth in mobility over the past 20 years.

In broad terms, the total number of internationally mobile students in tertiary programmes increased from 2 million in 1998 to 5.3 million in 2017. This works out to an average annual growth rate of 5% over this period, and, with the exceptions of some spikes in growth in 2002/03 and 2014/16, there is a surprisingly consistent growth pattern over nearly two decades. Following “slight levelling off in long-term trends” in 2012, growth resumed in 2014 with a 7% increase in the the total number of mobile tertiary students. “The number of international students began increasing again in 2014 and the years that followed, with annual increases of 8% in both 2015 and 2016. In the last year with available data, the growth was slightly more moderate, returning to 5% between 2016 and 2017.”

The hopeful note there is of year-over-year gains potentially returning to historical norms after a period of more sluggish growth in the first half of this decade.

For additional background, please see:

Most Recent

-

China in 2026: Slowing outbound student mobility, accelerating inbound momentum Read More

-

Surprise hike in international student visa application fees “a direct hit to Australia’s competitiveness” Read More

-

ICEF Podcast: “Good, steady, and disciplined”: New Zealand’s plan for sustainable international enrolment growth Read More