Market intelligence for international student recruitment from ICEF

2nd Aug 2017

Australia: Longer stays add up to 10% growth in ELICOS weeks

English Australia’s latest National ELICOS Market Report shows modest 2% growth in student numbers for 2016. This marks the fourth consecutive year of growth for Australia’s ELICOS providers (English Language Intensive Courses for Overseas Students), and comfortably moves the sector past the previous high point of 162,114 students in 2008.

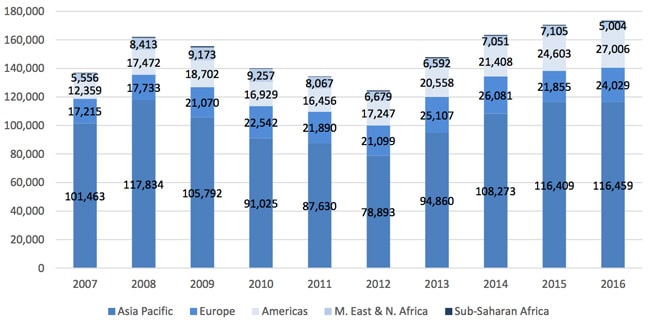

All global sending regions, with the exception of the Middle East, grew in 2016. As the following chart reflects, with Asian student numbers essentially flat it was really growth from Europe and the Americas that helped to offset a significant decline in Middle Eastern enrolments.

Total ELICOS enrolments by sending region, 2007–2016. Source: English Australia

But the real story for ELICOS providers last year is that that marginal growth in student numbers was greatly outpaced by a 10% growth in student weeks. Total ELICOS weeks amounted to 2,319,175 in 2016, up from 2,107,024 the year before.

Sending markets in the Americas accounted for roughly half of that growth in student weeks (+104,502). Asian markets, while more or less flat in terms of student numbers, accounted for much of the rest (+95,430 weeks).

The report adds, “In 2016, the average course length increased by a week to 13.4 weeks, generating a longer average course length than the most recent high of 12.9 weeks in 2013/14.” Reflecting these longer average stays, just over two-thirds of all ELICOS students held student visas in 2016, a slight increase in proportion over 2015 and the highest-ever level of student visa issuance in the sector.

These inter-related trends of increasing average course length and rising ratio of student visa-holders likely hold longer-term implications for international education in Australia. They suggest that a growing percentage of students may be planning further study in Australia after their language programmes.

Indeed, earlier research on the link between ELICOS and further education has found that the ELICOS sector is the pathway for two in every five international students in Australia’s tertiary sector. The same study found that almost two-thirds (63%) of international students who completed an ELICOS course in 2012 progressed to further study in another sector.

If those patterns hold true, then the underlying growth in ELICOS last year is very good news indeed for what is already shaping up to be another strong year for international enrolment in Australia.

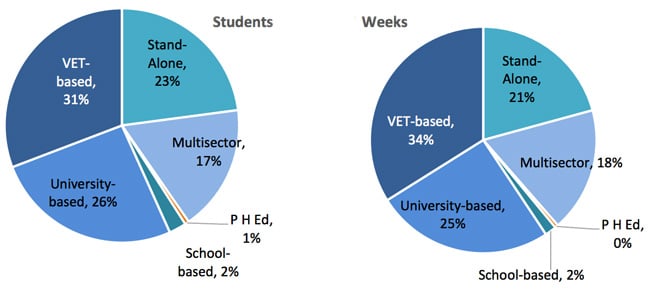

This connection between ELICOS enrolment and further education is further reinforced by a breakdown of enrolment by provider type included in this year’s report. As the following charts reflect, ELICOS programmes connected to vocational education and training (VET) institutions accounted for the largest proportion of enrolment, both in terms of student numbers and weeks, with university-based programmes following close behind.

2016 ELICOS enrolment, student numbers and weeks, by provider type. Source: English Australia

Top markets send three in every four students

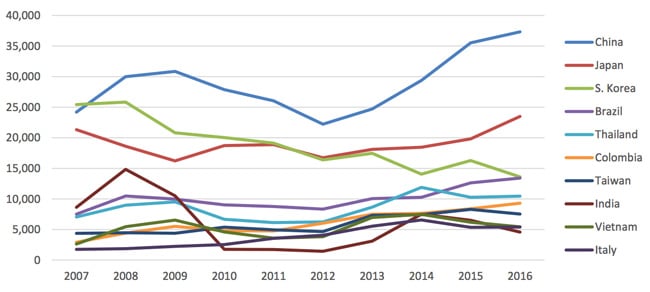

Australia’s top ten sending markets accounted for 75% of all ELICOS enrolments in 2016 (down slightly from 76% the year before), and, as usual, the table of leading markets reflects a mix of ups and downs during the year.

Top ten source countries for ELICOS in Australia, 2007–2016. Source: English Australia

Four of the five fastest-growing markets for the year are found within the top ten. Japan leads the group with a 19% increase in student numbers which helped to offset year-over-year declines from other Asian top ten senders, including South Korea (-16% enrolments in 2016), Taiwan (-9%), Vietnam (-12%), and India (-30%).

Outside of the top ten senders, Saudi Arabia also registered as one of the biggest declining markets for 2016. Its 38% decline in student numbers was the major factor in the Middle East being the only global region that didn’t grow for ELICOS providers last year.

On the positive side of the ledger, Brazil and Colombia – with 6% and 11% increases in student numbers respectively – played a big part in driving growth among the top ten senders, and in the notable increase in student weeks from the Americas.

English Australia estimates the total economic impact of the ELICOS sector at AUS$2.3 billion in 2016 (US$1.8 billion). This reflects both tuition and non-tuition spending, and represents an 8% increase over the estimated impact for 2015.

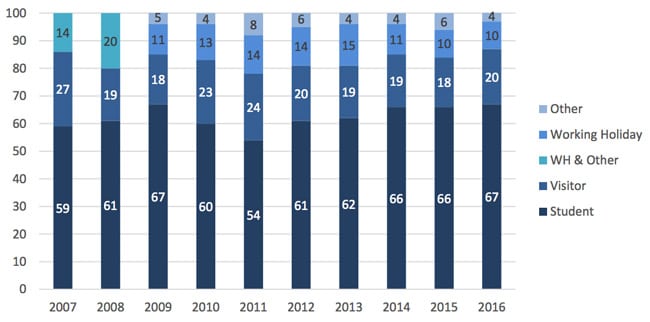

Editor’s note: There are significant differences between the sector-wide numbers reported in English Australia’s national report and the ELICOS statistics provided earlier this year by the Australian Department of Education and Training. This is accounted for in large part by the fact that the English Australia numbers include both students on study visas and those enrolled with other visa types. As the following chart illustrates, roughly a third of ELICOS students hold something other than a student visa during their term of study. ELICOS enrolment by visa status, 2007–2016. Source: English Australia

For additional background, please see: